Gold recently completed thedeath cross, when the 50 day moving average crosses the 200 day moving average. While I don’t put much faith in simply following technical indicators, I do use them as supporting evidence to justify a trade. I look for the fundamental story first, and then wait for the technical indicators to validate my theory. In mid-February I published an article making a bearish case for gold, and since then, the case has only become stronger. The general theory I outlined was that gold wasn’t trading at its current level because of a fear of inflation, but instead fear itself and investors were using gold as a safe haven investment. Investors are using gold as a substitute for treasury bonds. If treasury bonds aren’t paying much in interest, why not hold gold? Gold at least has the comforting aspect of being something real and can be physically held in case of Armageddon. The theory I outlined was that economic strength would drive interest rates higher, and unlike past market cycles, higher interest rates would be welcomed by the equity markets and signal a return to “normalcy.” The return of hope, growth and optimism will represent the end of the gold bull market. That however will not happen overnight, and it won’t be a nonstop flight, but the free market capitalism on which America is built has never failed us in the past. Like a Phoenix, the American system has always emerged from the ashes stronger and better, and if history tells us one thing, it is hope and optimism always prevailed in the long run.

Gold recently completed thedeath cross, when the 50 day moving average crosses the 200 day moving average. While I don’t put much faith in simply following technical indicators, I do use them as supporting evidence to justify a trade. I look for the fundamental story first, and then wait for the technical indicators to validate my theory. In mid-February I published an article making a bearish case for gold, and since then, the case has only become stronger. The general theory I outlined was that gold wasn’t trading at its current level because of a fear of inflation, but instead fear itself and investors were using gold as a safe haven investment. Investors are using gold as a substitute for treasury bonds. If treasury bonds aren’t paying much in interest, why not hold gold? Gold at least has the comforting aspect of being something real and can be physically held in case of Armageddon. The theory I outlined was that economic strength would drive interest rates higher, and unlike past market cycles, higher interest rates would be welcomed by the equity markets and signal a return to “normalcy.” The return of hope, growth and optimism will represent the end of the gold bull market. That however will not happen overnight, and it won’t be a nonstop flight, but the free market capitalism on which America is built has never failed us in the past. Like a Phoenix, the American system has always emerged from the ashes stronger and better, and if history tells us one thing, it is hope and optimism always prevailed in the long run.

Recent headlines/videos help make my case:

1) “Gold Prices Inch Higher as Inflation Climbs,” states one headline. Inflation is finally showing up in the numbers and all gold does is “inch” higher? If inflation was truly the driving force, I would expect the response to be measured in more than “inches.”

2) The headline “Precious Metals Rise as Consumer Sentiment Sinks,” demonstrates that economic weakness drives gold higher, the opposite you would expect if inflation was the driving force.

3) “Gold Prices Gain as Dollar Pressure Mounts,” highlights how the U.S. dollar is a major force driving the price of gold, and as the economy strengthens, so should the U.S. dollar. A higher dollar should result in a lower price of gold ceteris paribus.

4) The Uptrend in Gold Is Broken, Next Stop Could Be $1000: Don Hays. This video is currently being featured on Yahoo and makes the exact argument that I’ve been making, that gold is supported by fear. There is also a nice technical review of gold and the video is well worth watching.

5) Will Cyprus Turn the Tide for Gold? This article is fresh to the newswire, released just hours before I submit this article, and highlights once again how gold is responding to fear itself not fear of inflation. Eventually inflation may become a factor if it ever develops, but right now, in my opinion inflation isn’t the driving force behind gold.

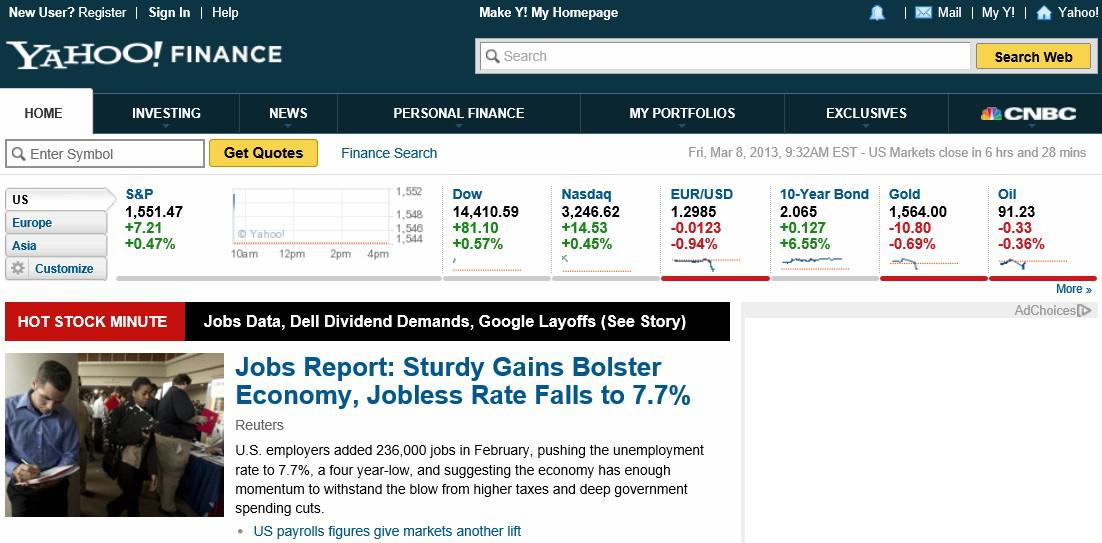

This graphic of the markets on the open after the release of the 3/08/13 jobs report highlights that theory in action.

(click to enlarge)

The jobs report was stronger than expected, pushing the unemployment rate down to 7.7%, 1.2% away from the rate identified by the Fed as the level likely to signal the end of its quantitative easing strategy. On this good economic news, interest rates as represented by the 10-year treasury, gapped up from under 2.00% to 2.06%. These higher rates however did not scare equities, as both the Dow Jones Industrial and S&P 500 drove higher. Gold on the other hand did not welcome the news, and sold off. Continued economic strength will likely result in stronger equity returns, higher interest rates, a strengthening dollar and the end of the Fed’s QE strategy. All those work against gold, which was down $10.80 on the news.

As the economy strengthens the main reason for holding gold, fear of Armageddon, becomes a distant memory. With a strengthening economy, the stars appear to be aligning against gold and Armageddon. Over a decade ago I remember reading a headline about how central banks were ending their sales of gold. Gold was around $250/oz, and gold had been in a multi-decade bear market. I was new in the industry and excitedly called my boss to let him know that we were seeing the bottom of the gold market. He probably just laughed, but in hind sight, that was the perfect indicator to identify the bottom of the gold market. Recently the headlines were that central banks‘ buying of gold was hitting a 48-year high. This sounds very bullish, but all that record buying did little to move gold in 2012, and the current level of the SPDR Gold Trust (GLD) is basically back to where it started 2012. GLD started 2012 around $151.99, and closed Friday at $154.00. It traded as low as $151.44 as recently as February 20, 2013. All that central bank buying did basically nothing to the price of gold. If central bank buying isn’t enough to drive gold higher, what will?

Hedge funds are selling gold, and as the realization that the reason they have been buying gold isn’t really a justification, that selling should accelerate. This video makes almost the identical case that I did last month in my bearish article. In my opinion, there is simply a fundamental misunderstanding of monetary policy. The Fed “printing money” simply does not necessarily lead to inflation. If it did, we would be experiencing hyperinflation right now, and we aren’t. As more and more people realize that, and learn to trust in the Fed’s ability to manage inflation, the major argument supporting gold will disappear.

Not only have hedge funds been selling, ETFs have been selling as well. GLD recently experienced its largest one-day outflow in 18 months. That event triggered the headlines “Could Gold ETF Outflows Drive ‘Vicious Circle of Selling?’” That event alone raises concerns about gold. Retail investors have been a major support for gold, and if their sentiment changes, the entire dynamic of the gold market will change, as will the Cable TV advertising lineup.

Not only have hedge funds and private individuals been selling gold, money managers have been actually shorting gold in record numbers. If there is such a thing as “smart money,” it isn’t just running for the exit, it has left the building.

The Fed released minutes recently suggesting that it may slow or end bond buying sooner than expected. Market expectations are shifting from QE Infinity to QE Ending. It was understandable to fear inflation when there was no end in sight to the printing press, and it appeared as if the money supply would grow forever, but that simply isn’t the case. I have always maintained that if there is one thing the Fed knows how to do, it is fight inflation, and I still maintain that belief. A well known adage of Wall Street is “don’t fight the Fed.” A bet on gold is a bet against the Fed, and its ability to contain inflation and maintain a stable U.S. dollar.

Fear that the U.S. dollar will collapse was also lessened recently. With the release of the Fed Minutes, the U.S. dollar had its strongest one-day gain in seven months. It is hard to make a case for higher gold prices when the U.S. dollar is going higher. Headlines of “Currency Wars” may sound frightening, but in reality a currency war would most likely result in a stronger U.S. dollar, rather than a weaker one. We have the currency the rest of the world would be going to war against, and it is hard to imagine the U.S. dollar weakening against all other currencies when those countries aren’t concerned with maintaining their status as the world’s reserve currency, or the long-term credibility of their central bank and stability of their currency.

I’ve been working on this article since mid-February. I was about to remove this last paragraph, but decided to leave it is as a quote as if it had been published at an earlier time. I was writing about how gold was responding to some current news. The key point was that gold sold off with equities, and bonds held steady. It reviews the dynamics that exist in the equity, bond and commodity markets today.

Lastly, while gold sold off today along with the broader markets, bonds held steady. The ten year treasury rate was essentially unchanged. Unlike holders of gold, holders of treasury bonds did not lose money today. Treasury bonds retained their safe haven status. More troubling for gold however is that interest rates didn’t change much. Normally when equities sell off to this extent interest rates fall, as money flows from equities into bonds. Today rates simply held steady. That may imply that a floor is being put in for the ten year treasury at 2%, and rates may be going higher from here. If that is the case, I would expect selling of gold to continue as people seek the safe haven and higher yield of treasury bonds. As I highlighted in my previous article, gold has been behaving like a leveraged long bond. While both treasury bonds and most likely gold will lose money as rates go higher, gold will likely lose more, and it doesn’t have the yield to cushion the fall back on.

With the Dow making new highs, equities, especially the dividend payers that make up the Dow Jones Industrials, will offer solid returns and yields to compete against gold. As equities march higher, selling of gold will likely be part of what fuels the advance forward. People talk about the Dow and other equity indexes having a P/E similar to what they were before the 2008 crisis, and that the markets are fully valued. I disagree with that conclusion simply because before the 2008 crisis we had interest rates above 4%, now they are just breaking above 2%. A P/E of 14 when interest rates are over 4% is a lot different from a P/E of 14 when interest rates are at 2%, and growth prospects are increasing, not decreasing.

In conclusion, many of the pillars that have been supporting gold are weakening. If my theory is correct that the Fed’s monetary policy has been and will continue to be successful in maintaining inflation, gold may have already seen its best days, at least for this cycle. As the economy slowly regains its footing, interest rates should head back toward their norms. As this happens, bond yields will present an attractive alternative to holding gold. Continued economic strength should also lesson the safe-haven appeal of gold as the fear of Armageddon fades in our memories. Ironically, if mild inflation does emerge, which I expect will eventually happen, gold will likely sell off even further as the impact on interest rates provides a greater incentive to buy bonds than mild inflation does to hold gold. Gold has already discounted a tremendous amount of potential inflation. Inflation that is unlikely to materialize in my opinion, at least not to the extent that would support gold at levels higher than they were during the double-digit spiraling inflation of the 1970s. Today $1,591 will buy you a wheat thin sized wafer of gold; back then, when inflation was real, it only took about $750.