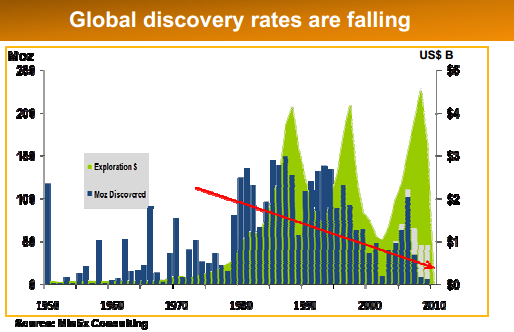

The lead time from discovery to a producing mine is typically 10 to 15 years unless it’s already very near a producing district or mine, as you can see on the following chart from the European Gold Forum. The chart shows there were three large exploration cycles in the last 30 years. The last cycle resulted in only a modest spike in ounces between 2004 and 2007, before fizzling out. Of the small universe of quality advanced stage deposits in the sector, many are from this period.

Meanwhile, exploration or greenfield budgets have completely collapsed, and virtually no new discoveries are being made. The exploration that is still taking place is follow-up on previous high-value discoveries and targets. There’s little speculative exploration going on right now.

Most firms still in the field are operating on capital raised before the sector crashed. Many investors who had provided that capital have relentlessly dumped their shares and no longer care about the outcomes of the explorations or mines they funded. With few exceptions, most of the discoveries of the 1980s and 1990s are already producing and, in many cases, depleting. On advanced-stage projects, the majors try to get little toeholds of 10-15% in exchange for cash. There are some metal stream deals in place for smaller capex mine construction. This can be a win-win situation, without badly diluting shares.

(click to enlarge)

There’s little capital for developing new production. The few large new mines that are coming into production, such as those owned by Detour Lake, Osisko (OSKFF.PK), G-Resources (GGPXF.PK) and Allied Nevada (ANV), trade at valuations below the capex of their brand-new, state-of-the-art mines. That means all-in costs at current valuations are already sunk, and thus are meaningless for today’s investor (see the “Golden Rule“). There is zero value being attached to the deposits in these particular cases. Even without the potential blue sky from metal prices, the valuations put on these precious metal properties as an asset group are as undervalued as any I have ever witnessed in any sector in the last forty years.

If mid-tiers and majors are to continue as going concerns, as opposed to liquidating royalties, then the existing and remaining discoveries from between 2004 and 2007 and late 1990s cycles must be purchased and developed. I suspect this will begin to happen, and there may be whole new firms and entities coming forward to do it. Right now, the best properties could be scarfed up for a nominal amount of capital. In today’s central-bank-infected, maladjusted world — where investors are buying houses to rent to poor people in U.S. cities for a 4% cap rate (see“America’s New Landlords”) and collecting 6% on Rwandan bonds (see “Illusion of Safety Leading to Minsky Moment“) – it makes zero sense that gold deposits are trading at 30% or less of net present value (NPV) and over 25% IRR.

Further the cost curve is now bending in the direction of building production more economically because of the immense overcapacity in China for key materials that go into mine development and production. I have discussed this in (Mining Costs are Falling). I’ve been putting in calls to companies over the few week to verify this. In the European gold forum, it was alluded to by some of the presenters. In particular, listen to the descriptions by Detour Lake and Osisko (4:00-6:30 mark) concerning recent labor, contractor and materials costs. Reading between the lines, one can expect some positive surprises on the operating side.

The list of selective deposits for new mines is not large. There is simply a limited supply. My sense is that someone with $2 billion in cash and a billion-dollar credit line could create the spark for the next gold mining powerhouse from this baby-out-with-the bathwater stable. Despite a non functioning “market,” and chasing of low-return rainbows, there are still some serious investors left for this to take hold, even without higher POG.

I leave you with a commentary from Seth Klarman, who has positions in many of the stocks I use, and has one of the best long-term track records in the markets. He typifies my approach and philosophy:

“Only a small number of investors maintain the fortitude and client confidence to pursue long-term investment success even at the price of short-term underperformance. Most investors feel the hefty weight of short-term performance expectations, forcing them to take up marginal or highly speculative investments that we shun.

Our willingness to invest amidst failing markets is the best way we know to build positions at great prices, but this strategy, too, can cause short-term underperformance. Buying as prices are falling can look stupid until sellers are exhausted and buyers who held back cannot effectively deploy capital except at much higher prices.

Short-term underperforrnance doesn’t trouble us; indeed, because it is the price that must sometimes be paid for longer-term outperformance, it doesn’t even enter into our list of concerns. Patience and discipline can make you look foolishly out of touch until they make you look prudent and even prescient. Avoiding leverage may seem overly conservative until it becomes the only sane course. Concentrating your portfolio in the most compelling opportunities and avoiding over diversification for its own sake may sometimes lead to short-term underperformance, but eventually it pays off in outperformance.”Source