Precious Metals Weekly Market Wrap

A reversal of the recent strong dollar trend, due in large part to perceptions of a more dovish Federal Reserve, contributed to the biggest weekly advance for precious metals in nearly two years. On Wednesday, Fed Chairman Ben Bernanke said that:

highly accommodative monetary policy for the foreseeable future is what’s needed in the U.S. economy.

and that was all traders needed to bid gold and silver prices sharply higher.

Short-covering was no doubt a key driver of recent gains as were recent developments in China that included higher than expected inflation, strong physical demand, high premiums, and record trading volumes in Shanghai. Here in the U.S., physical demand has also been strong as evidenced by multi-year highs in the cost of borrowing gold, and COMEX gold stocks that reached their lowest level in more than a decade.

Gold ETF outflows have been accelerating in recent weeks, however, and it is not at all clear whether recent developments will be enough to turn bearish futures market traders and U.S. money managers back into gold bulls.

For the week, the gold price jumped 5.1 percent, from $1,222.00 an ounce to $1,284.80, and silver surged 5.5 percent, from $18.88 an ounce to $19.92. Gold is now down 23.3 percent in 2013, some 33.2 percent below its all-time high of over $1,920 an ounce almost two years ago, and the silver price has fallen 34.4 percent this year, almost 60 percent below its record high near $50 an ounce reached 27 months ago.

As he has done many times, Bernanke caused asset prices to move sharply higher last week, however, as noted in Short-Timer Bernanke Unwittingly Boosts Gold Price on Thursday, all one has to do is look closely at Bernanke’s remarks to realize that they were widely misinterpreted. The often repeated phrase quoted in the first paragraph above was in reference to short-term interest rates, not the “tapering” of central bank money printing that has roiled markets in recent months.

Yes, there was a comment about “push back” if “financial conditions were to tighten”, but that’s a rather nebulous promise on which to base a trade as opposed to a direct reference to policy.

Once asset prices began to rise, however, few traders or investors seemed interested in discovering the true meaning of the Fed Chairman’s remarks. But, that’s why gold and silver had their best combined week since late-October of 2011, a move that did little to reverse deep losses for both metals in 2013.

In this article at the Telegraph, Ambrose Evans Pritchard echoes the view that markets misinterpreted Bernanke’s comments, going so far as to say:

Bernanke has not retreated from monetary tightening. The Fed is still on track to start tapering bond purchases as soon as September … the $40 surge in the price of gold is likely to be reversed in short order.

A falling gold price and tapering of the Fed’s money printing effort in two months are anything but certain, but key data points that are surely worth paying close attention to at this juncture are gold ETF flows. Outflows from the SPDR Gold Shares ETF (GLD) had been accelerating leading up to Bernanke’s comments on Wednesday with some 23 tonnes exiting the trust early last week, and it will be important to see if the Fed Chief produced any change in sentiment amongst mostly bearish U.S. money managers.

Holdings at the iShares Silver Trust ETF (SLV) jumped by another 134 tonnes last week and are now actually 100 tonnes higher than where they began the year in what continues to be a puzzling development as detailed in The Curious Case Of Physical Demand For Silver Versus Gold.

Given the failed test for gold at $1,300 an ounce last week, I wouldn’t be surprised to see this rally prove to be short-lived but, over the long-term, there are still many reasons to remain bullish, most of them now originating in China.

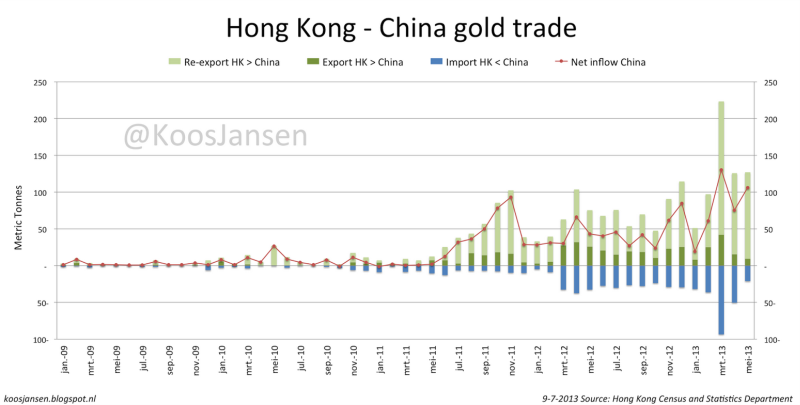

The Hong Kong Census and Statistics Department reported early last week that net gold exports to mainland China rose from 80 tonnes in April to almost 109 tonnes in May, this following a record high of 136 tonnes in March. As shown in the graphic below via Koos Jansen, this is simply unprecedented demand that, if continued, will surely have a positive impact on the gold price.

(click to enlarge)

Record trading volumes were seen last week on the Shanghai Futures Exchange when after-hours trading was launched and the combination of strong demand for the physical metal and tight supply have kept premiums high. China is expected to import about 1,000 tonnes of gold this year through Hong Kong alone which, combined with domestic production of 400+ tonnes, will make them the world’s biggest gold consumer by far, taking that title away from India where draconian measures by the government to limit gold imports have begun to have an impact.

In this article at Mineweb, Lawrence Williams summarized the situation in China nicely:

But if the demand continues at this kind of level, with stocks of physical gold continually moving from vulnerable western hands to more stable eastern ones then at some stage there will be a very apparent shortage of physical metal in the West. Increasingly gold trading will move from exchanges like COMEX to Shanghai and Hong Kong. COMEX may become an effective irrelevance in the gold market dealing only in ‘paper’ gold (which it effectively is already) and the physical gold price momentum will move to the east. Currently it is COMEX which is setting the global gold price. In the future it will be Shanghai if the current trend continues – and then it will be a wholly different ballgame!

Signs of big changes underway on Western metal exchanges were apparent last week when COMEX registered gold stocks fell to a 12-year low of less than one million ounces. This is an ongoing trend that has not let up in recent weeks and, if continued, could have a big impact on prices.

Also, gold lease rates are now at their highest level since the depths of the financial crisis in early-2009, another indication of relatively tight supply for the physical metal in the West, due in part to physical metal being shipped to Asia in recent months. Gold forward rates, also known as “GOFO”, offered by bullion banks and central banks to institutional investors and gold users, moved into negative territory for the first time since late-2008 indicating a shortage of physical gold available in the market.

This is all part of the developing trend that began early in the year and then accelerated in April when the gold price tumbled below $1,500 an ounce for the first time in two years. Asian buyers stepped in to take advantage of lower prices and, in the process, spurred a flow of physical metal from the West to the East whose impact has yet to be felt in the Western markets where, for the time being at least, the gold price is set.