The main determinant of asset prices in recent years has been the level of long term real interest rates, which remain remarkably low, and are expected to remain remarkably low for some considerable period.

When you’ve got such low long term real interest rates, asset prices, all asset prices, will inevitably be high. And on that basis, as the Committee explained, very clearly before the crisis, it’s not surprising that if people feel that asset prices, particularly house prices, are likely to remain at this high level – it’s not a question of expecting them to rise further, I think that’s gone, clearly; but they’re not expected to fall sharply…

The reason for concern in the future is not the current configuration of interest rates and asset prices; it’s that we know that at some point real interest rates have to get back to a healthier and more normal level. Positive real interest rates are crucial for the successful operation of a market economy. The real challenge is to navigate our way back to that level.

Once real interest rates are back to that level then you would expect to see some consequences for asset prices, possibly falls in asset prices. And at that point it will be important that people have had time to deleverage and to get to a point where their degree of indebtedness is not such that they find themselves in deep financial trouble when asset prices fall. – Former Bank of England Governor Mervyn King during the Q&A section of his final Inflation Report, May 15, 2013.

When King uttered these words in his final Inflation Report as Governor of the Bank of England (BOE), there was no sudden surge in interest rates or sell-offs in financial markets as we saw when one week later Federal Reserve Chairman Ben Bernanke seemed to suggest that the Fed was getting ready to start the process of normalization. Yet, no one in the press conference questioned King’s premise.

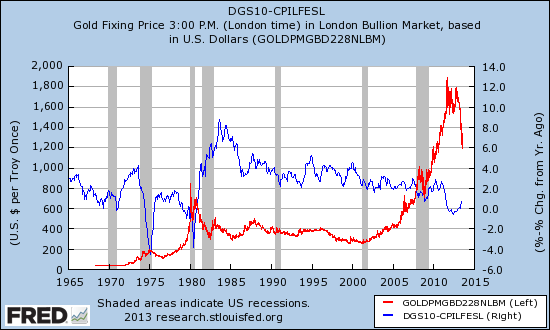

Assuming gold is an asset, its price seemingly violates this simple relationship. In the graph below, I juxtaposed data available from the St. Louis Federal Reserve: the price of gold, the consumer price index (excluding food and energy), and the 10-Year Treasury Constant Maturity Rate as a proxy for long-term interest rates. I constructed an approximation of real interest rates by simply subtracting the year-over-year change in the CPI from the 10-Year Treasury rate. The graph shows gold in red and the real interest rate in blue.

(click to enlarge)

Gold’s price has had an inconsistent relationship with real interest rates

Source: St. Louis Federal Reserve

While it is possible to explain the rapid rise in gold since 2005/2006 as an anticipation of negative real rates, it only took a small reversal in real rates to generate a rapid collapse in gold’s price. Inconsistent relationships like these form the crux of a larger conceptual dilemma that authors Claude B. Erb and Campbell R. Harvey (Duke University, National Bureau of Economic Research) attempt to tackle in a May 2013 paper called “The Golden Dilemma.” This paper is a comprehensive examination of the various reasons offered to buy gold. The authors systematically undermine almost every reason. I found the paper interesting and compelling enough to offer up my own summary and critique of it. In particular, I take issue with the failure of the authors to address the biggest elephant in the room: unprecedented easing and accommodation in global monetary policies. To me, these actions truly define a “new era” in financial markets that justifies investments in gold. The Golden Dilemma is a very long paper, but I encourage my fellow gold bugs to give it a glance and a chance.

With gold prices steadily falling over the past two years, it has been much more difficult to be a gold bull. I am in the habit of reaffirming my bullishness and justifying my opportunistic accumulation. However, the recent hike in interest rates and the market’s initial negative reactions prompted me to examine some postings by deflationists who continue to believe that asset prices are heading for another monumental collapse. I stumbled upon “The Golden Dilemma” during one of my rummaging expeditions.

Erb and Harvey (the “authors”) take on the task of deconstructing six reasons gold bulls commonly offer up for buying gold:

- protection against inflation

- protection against currency debasement (my favorite)

- alternative to assets with low real returns – attractive when rates are low

- safe haven (a reason I have never liked)

- preparation for a return to the gold standard (my least favorite)

- contrary position in an underowned asset

.

After digging through a mountain of data, Erb and Harvey conclude that gold is extremely over-valued although it could still go higher due to the purchases of central banks, particularly in emerging markets. The “dilemma” facing investors comes from assessing whether gold will revert to “the mean” based on historical relationships to inflation, disposable income, and GDP or whether a new era has arrived that justifies the high (and higher) valuations.

While the authors spend a lot of time wrestling with historical data in interesting ways, they spend little time assessing what gold bulls see as the core of a “new era”: a Federal Reserve since Alan Greenspan that is willing to debase the currency and otherwise implement extremely accommodative monetary policy in order to fight any and all economic malaise. Monetary policy since the financial crisis of 2008-2009 is well recognized as operating on an unprecedented scale and scope. There exists what I think is a justified belief that the Federal Reserve is willing to tolerate much higher inflation as an alternative to its bigger fear: deflation. (The other wildcard is whether the Fed believes it must keep rates low to facilitate cheap borrowing for the Federal government. Much higher rates could facilitate a funding crisis).

Regardless, I think the paper’s arguments warrant examination because some of them provide sobering reality checks for us gold enthusiasts. Basically, if the Federal Reserve actually manages to unwind accommodative policy well-ahead of an inflationary threat, then gold should, in all likelihood, tumble back to some level in line with historical patterns.

The authors clearly think that the high value of gold is essentially the product of a few, dedicated buyers who are taking advantage of their ability to drive the market higher; buyers who buy just because the price is moving upward:

While the possible value of all the gold ever mined is about $9 trillion, only a small amount of gold actually trades in financial markets. We show that the investment demand for gold is characterized by positive price elasticity. This is one way of referring to momentum investing. As a result, even though historical measures of “value” might suggest gold is very expensive, it is possible that the actions of a relatively small number of marginal, momentum, buyers of gold could drive the real and nominal price much higher (especially if the marginal buyers are not focused on ‘valuation’).

Since almost no one buys an asset with the hope or expectation that its price goes down, momentum investors can be thought of as the most exuberant investors/traders in the pool. I would argue that the number of people willing to buy an asset as its market value is plummeting is similarly small. In other words, the positive price elasticity is no surprise in financial markets. So, the main question is who knows the valid valuation metric. The authors talk about a bet on gold as a bet on future price appreciation. I contend this is nothing unique or surprising:

The real price of gold may or may not mean revert over time, but the purchasing power of gold is driven by changes in the real price of gold. An investment in gold is a bet on the future evolution of the real price of gold, whether an investor is aware of the bet or not.

Protection against inflation

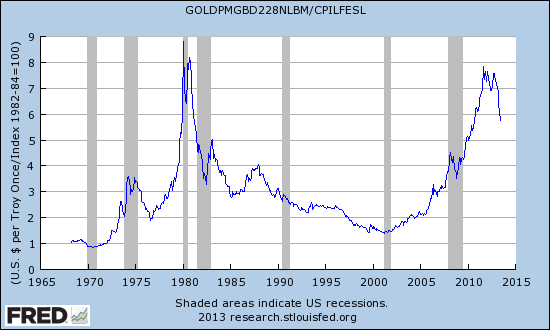

With that, let’s start from the top of the paper’s arguments. The authors argue that gold has served as a poor hedge of inflation. They demonstrate this by simply dividing the price of gold by the Consumer Price Index [CPI] excluding food and energy. I reproduce this chart using data from the St. Louis Federal Reserve to get the latest relationships and provide a way for you to review the data for yourself. (You should be able to click the links referencing the St. Louis Fed as a source to go directly to my customized graphs and play with the data for yourself).

(click to enlarge)

The real price of gold has changed dramatically during well-defined periods

The monthly average of this ratio through June 2013 is 3.0 and the latest monthly value is 5.7. Both inflationists and deflationists agree that the CPI is a poor measure of real inflation. Inflationists contend the CPI is too low especially because of hedonistic adjustments to take into account the quality of goods. Deflationists contend the CPI over-estimates real inflation because it does not adequately take into account the improved quality and performance of goods. I will call it a draw and use the data that are readily available and most widely accepted.

If gold hedged the CPI, the ratio of gold to the CPI should be relatively consistent. Instead, gold is 90% above the historical average. The authors argue that this divergence represents a serious disconnect in valuation. I do not think this average is meaningful. Instead, I think it is more interesting to think of gold as moving in three distinct phases in the past 40+ years: a rapid run in response to the inflationary 1970s, a steady decline for twenty years as inflation rates came down, and finally another rapid run-up as the U.S. dollar index experienced a new secular decline. I will cover this in more detail later.

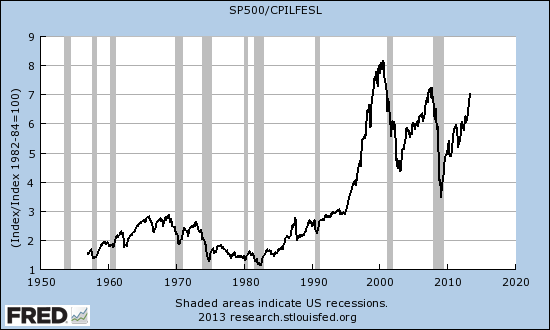

Moreover, investing in the stock market is often cited as a way to hedge against inflation. The relationship of the S&P 500 (SPY) to inflation has been even more erratic than gold’s relationship to inflation.

(click to enlarge)

The S&P 500 has had a very volatile relationship to inflation

Source: The St. Louis Federal Reserve

After seeing THIS graph, I might be tempted to say that the S&P 500 is wildly over-valued given in the mid-1990s its historical relationship to inflation dramatically changed with an impressive breakout. An overall generational decline may well be underway given the dramatic series of lower highs and lower lows since the peak of the stock market bubble in 2000. I will leave that analysis for another time. My main point is that the market’s concern about inflation appears to fluctuate given everything else the world offers as matters of concern; it is not consistent. So just how much inflation gold should hedge is certainly up for interpretation.

So how about hedging expectations of inflation? Perhaps there is just a lag in the gold price of some unknown length to realized inflation. That argument certainly would not work for the past since the realized inflation rate has been in a steady decline. Indeed, the authors show absolutely no relationship between gold and a measure of “unexpected inflation.” I interpret this to mean that the gold market is no better than any other market at anticipating the realized rates of inflation.

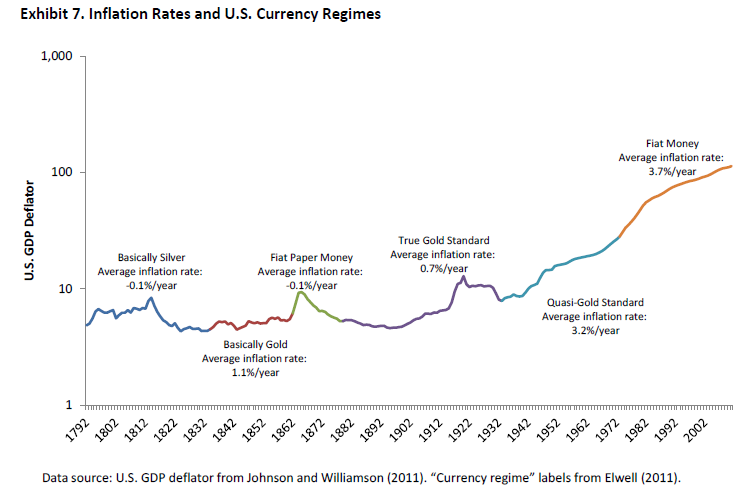

The authors go the extra mile by reaching far back into history to cobble together rough approximations of inflation since the early years of the U.S. They overlay these data with the different currency regimes in place at the time. The chart below shows no correlation between the currency regime and the inflation rate. For the sake of space, I refer the reader to the paper to review the specific definitions.

(click to enlarge)

Inflation Rates and U.S. Currency Regimes Since 1792

Based on this representation, fiat money and the gold standard have not had distinctly different impacts on inflation rates. Something else is more important for driving inflation rates. The authors take this analysis as further proof that gold is a poor hedge against inflation.

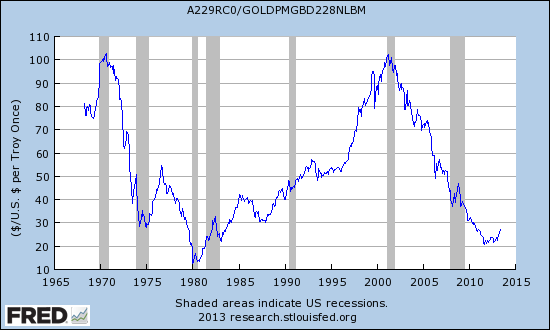

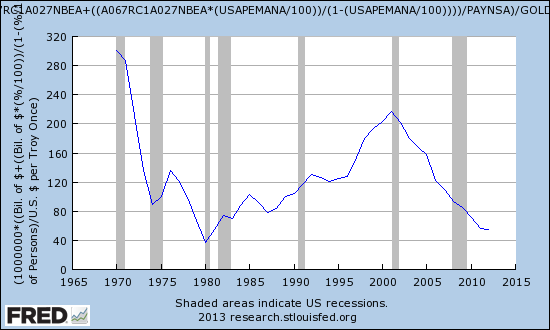

The authors also created a valuation metric I had never considered before: the value of disposable income measured in gold. They provide a chart of U.S. disposable income per capita priced in gold. This view shows gold is almost as expensive as it was in 1980, a view consistent with the real price of gold shown earlier. I reproduced the graph using St. Louis Federal Reserve data and added a second confirmation using the U.S. disposable income per non-farm employee priced in gold. The disposable income data are only available annually. I used the average employee and average gold price in the ratios. I also had to add in the non-farm and farm employees for an approximate total – employees include part-timers.

(click to enlarge)

U.S. Disposable Income Per Capita Priced In Gold

Source: The St. Louis Federal Reserve

(click to enlarge)

U.S. Disposable Income Per Employee Priced In Gold

Source: The St. Louis Federal Reserve

(Note that the authors have a dataset allowing them to go back 90 years. Their chart shows a stagnation of disposable income priced in gold since the 1930s.)

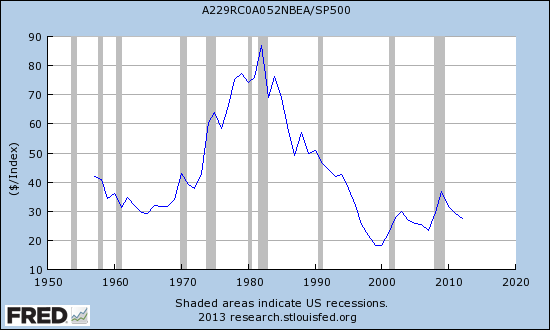

There is a potential flaw in this view that is exposed by measuring disposable income per capita in terms of how much money it takes to buy a share of the S&P 500. The graph below suggests that the S&P 500 was extremely expensive at the beginning of the great bull market that started in 1982. Moreover, as the market approached its destiny with the historic crash in 2000, the market got ever cheaper – suggesting that normal folks should have been chasing the rally and buying more and more shares. (Again, the S&P 500 is measured as an average value for the year and divided by income earned for the year).

(click to enlarge)

U.S. Disposable Income Per Capita Priced In S&P 500 Value

Source: The St. Louis Federal Reserve

Protection against currency debasement

This decline in the value of income makes sense to me when I think of the debasement of the dollar since 2000. Yet, even when it comes to using gold as a hedge against debasement, the authors find a way to debunk it. This is where I disagree the most.

The correlations are confounded because a lot of things move currency values in the short and long run. The market’s willingness to value one currency against another in any “rational” way also varies. Just look at the constant pleas of central banks in Switzerland, Japan, and Australia about the excessively high valuation of their respective currencies over the past few years. So, it is no surprise when the authors take the extended historical data and find no correlation between gold and the U.S. dollar (UUP). However, I am much more interested in the way in which gold HAS moved directly in relation to the dollar index since the dollar hit a peak in 2000.

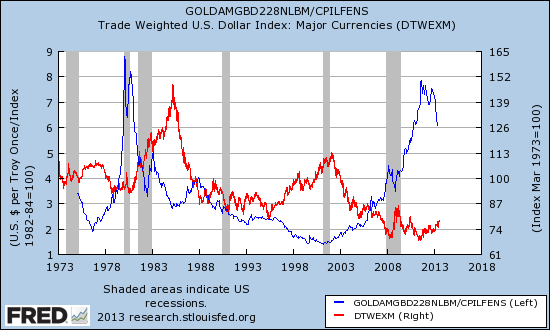

The authors confuse the issue by examining gold as a hedge against anycurrency. The authors conclude that the price of gold is high in the local currencies of the Australian dollar, Canadian dollar, (theoretical) Deutsche Mark, Japanese yen, New Zealand dollar, Swiss Franc, the British pound, and the U.S. dollar. Almost none of these surprise me since currency debasement has become a de facto matter of monetary policy. Given the U.S. dollar is the world’s reserve currency, its relationship to gold should be considered the most important over all others. In fact, it was the precipitous decline in the dollar since 2000 that finally convinced me in 2004 to get serious about buying gold. Using data available from the St. Louis Federal Reserve, I compare the real price of gold (gold divided by the CPI excluding food and energy) versus the trade-weighted dollar index against major currencies (the broad index only goes back to 1995).

(click to enlarge)

The real gold price has generally trended with the inverse of the trade-weighted U.S. dollar index

Source: The St. Louis Federal Reserve

Until the financial crisis, the real price of gold (and the nominal actually) roughly followed the inverse of the value of the dollar index. There was a mild exception between 1989 and 1996. When the dollar weakened coming out of the crisis, gold took off in near-parabolic form, presumably as other fears and concerns encouraged newly motivated buyers to come into the market. When the dollar bottomed out in 2011, gold reached a peak. It was a peak far removed from where the dollar had previously bottomed. I do not feel equipped to make a valuation argument based on these data, but I do recognize that based on these relationships, gold has far exceeded its recent history as a hedge against dollar debasement. The recent correction in gold reflects some combination of strengthening confidence in the U.S. dollar and the recent sharp spike in interest rates. Regardless, I think it is a mistake to think that in generalyou cannot expect gold to get cheaper with a stronger dollar and vice versa just because the precise magnitude for the relationship is elusive.

Alternative to assets with low real returns – attractive when rates are low

I had not heard the interest rate argument phrased as implying gold serves as an alternative investment. It is essentially an argument that gold prices should go up when real interest rates fall. This assumption when applied to assets underlies King’s quote that began this piece. The authors do find a strong correlation between the real yield of the 10-Year Treasury Inflation Protected Security (TIPS) and gold starting in 1997 when these TIPS were introduced.

From here, the authors go on a strange journey that casts doubt on the sustainability and applicability of any relationship in financial markets. They go on to show a low correlation between gold and interest rates in the United Kingdom (of course there must be SOME country where the correlations fail for SOME reason).

The authors also note that gold is highly correlated to time. This is an odd detraction given that, as shown above, such an assumption can fail spectacularly for many years. Moreover, one could argue the stock market is highly correlated with time (it has trended upward over the long term), but this would hardly be accepted as a reason to avoid investing in it or doubting its value.

Safe haven

I have never liked the “gold as a safe haven” argument. I have come to think of the financial markets as full of risks where nothing is truly safe. Any investments or trade is a risk that requires management, sometimes with different techniques. In Armageddon, one of the last things I will worry about is how much paper money (or gold) I still have in my pocket or in a vault far away. Add to this reality gold’s sorted history of government regulations, including price-fixing and confiscations, one cannot seriously consider gold a safe haven in the traditional sense of the word. It has its own set of special risks. The authors of course liberally reference these and related risks as additional flaws in the gold thesis.

The latest financial crisis was a reminder that gold cannot at all times be a safe haven. As liquidity dried up across the global financial system, gold collapsed in price. For example, in October 2008 gold priced in dollars lost 20%. This collapse proved to be the last great buying opportunity for gold. Nonetheless, it did not behave as a safe haven should.

The authors focus on hyperinflation as the main calamity that might motivate a bet on a safe haven. The fear of hyperinflation actually combines multiple reasons for owning gold. The authors reference the Brazilian experience with hyperinflation and seem to suggest that nothing can perfectly hedge against hyperinflation. In Brazil’s hyperinflation, gold did retain its value better than paper money. I consider this at least a partial victory for hedging against currency debasement. Of course the authors interpret this episode only as a complete failure of gold to deliver a perfect safe haven.

Preparation for a return to the gold standard

Next, the authors take on the idea that gold will one day again replace paper money as a currency. The authors link the idea of gold as money to the establishment of a gold standard. I think gold should be able to co-exist as money along with other currencies, and I certainly am not holding out hope that a gold standard will return.

The most interesting part of this argument occurs when the authors claim “…in the U.S. there has been an abundance of research that finds little evidence of a link between money supply growth rates and inflation rates” and provide one related reference: Anderson, Richard G., Robert H. Rasche and Jeffrey Loesel. 2003. “A Reconstruction of the Federal Reserve Bank of St. Louis Adjusted Monetary Base and Reserves.” Federal Reserve Bank of St. Louis Review, (September): 39-69. In an EconTalk interview on January 17, 2011 (“Boudreaux on Monetary Misunderstandings“), Don Boudreaux of George Mason University, recounts how inflation used to mean specifically an increase in the money supply. He goes on to say (emphasis mine):

In fact, inflation today means, to the average person here, even the typical well-informed professional economist who uses it, not an increase in the money supply, but a sustained increase in the general price level-a sustained increase in average prices. But it’s important to remember what inflation originally meant, because there’s a connection of course between changes in the money supply and changes in the price level…Inflation becomes salient, becomes a meaningful and interesting concept to study when we recognize that prices are changing not because of any changes in real resource constraints, real consumer demands in the economy, real shifts in consumers’ preferences for savings as opposed to consumption-but changes simply caused by exogenous increases in the supply of money.

So, I hardly think that the connection between the money supply and inflation is a settled matter amongst economists.

The reported lack of evidence that appears in a paper from the St. Louis Federal Reserve is also ironic. Just thinking anecdotally, it sure seems that central banks are willing to evoke the money supply as a theme of monetary policy. For example, the Bank of Japan is definitively increasing its money supply to help drive inflation higher. Ben Bernanke has been careful to explain that quantitative easing (QE) is not the same as printing money since it does not add currency into the money supply. He mentions this to calm fears that QE will lead to rampant inflation. Here isa quote from the New York Federal Reserve in a piece describing Large Scale Asset Purchases (LSAPs are colloquially also referred to as QE):

Most commonly used measures of the broad money supply include both currency and certain types of bank deposits, which in effect represent money created by banks when they make loans, but not reserves. These broad money measures tend to be more directly relevant for economic activity and inflation.

Once again, it seems there is reason to believe that money supply does impact inflation.

A contrary position in an underowned asset

Last but not least, the authors address the argument that gold is underowned. They primarily focus on the possibility for every investor to establish portfolios with a “market weight” in gold. Of course there is insufficient supply to meet that kind of demand. Unlike the stock market where shares can be instantly created to meet demand, gold cannot be so easily summoned into existence.

The examination of the supply side of this question takes a slightly bizarre turn when the authors consider the possibility of obtaining extraterrestrial and undersea sources of gold:

…there is considerable interest in near Earth asteroids given an important study by Brenan and McDonough (2009) that argues that much of the Earth’s precious metals are a result of asteroid collisions. The near-Earth asteroid 433 Eros might contain up to 125,000 metric tons of gold (see Whitehorse 1999). The website asterank.com catalogs 580,000 asteroids in our solar system and provides estimates of both the mineral value and the estimated profit from harvesting. There are currently 15 near-Earth asteroids with expected profit greater than $1 trillion according to the website. Closer to home, perhaps someday in the future someone will figure out how to implement Nobel prize winner Fritz Haber’s plan to electrochemically recover some of the estimated 8 million tons of gold in the world’s oceans (see Miller 2012).

The argument gets stranger still when the authors note that at current production rates, the United State Geological Survey’s (USGS) estimate of 51,000 metric tons of “exploitable gold reserves” will run out in 20 years. Such estimates are often tricky (especially if we soon grab gold from outer space or out of the water), but this prospect alone could serve as plenty of reason to accumulate gold at current prices. It would throw out the notion that gold needs to adhere to historic relationships when scarcity was not a salient issue. Instead, the authors use this statistic to argue that is then not possible for every investor to obtain a “market weight” of gold: there is not enough to go around. This reality seems more like an argument against the return of the gold standard and not an argument against owning gold. The laws of supply and demand should send gold’s price skyward if such scarcity appears while demand for gold continues to grow.

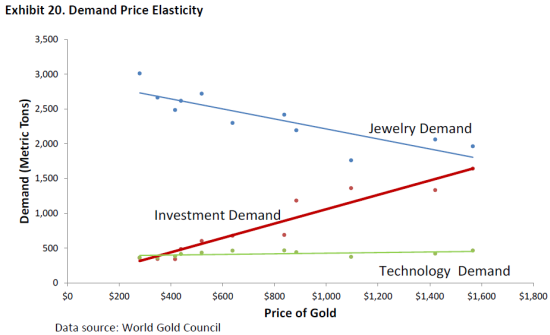

Indeed, the authors derive a positive sloping demand curve for investors to suggest that gold’s increasing price is the result of too much demand chasing too little supply in addition to momentum investors chasing higher prices.

(click to enlarge)

Demand Price Elasticity of Gold

Part of this upward sloping demand curve is expressed in the rising assets in the SPDR Gold Trust (GLD). Interestingly, the authors appear comfortable drawing a conclusive correlation between the real price of gold and the increased assets in GLD although GLD has only existed since 2004. These assets are now larger in size than China’s gold holdings. The authors imply that GLD is a primary channel for the excess demand that helps send gold prices higher. Central banks collectively represent another major channel for excess demand.

The authors conduct an interesting exercise to try to assess whether net central bank demand for gold is helping drive up gold’s price. They speculate over what could happen if the BRIC countries – Brazil, Russia, India, and China – attempted to buy enough gold to “catch up” to the U.S. or even Switzerland in terms of gold to GDP or population ratios. The resulting excess demand would be tremendous and likely pressure prices a lot higher. In China’s case, an interest in diversifying foreign reserves out of U.S. dollars might be enough to spur a lot more buying from China. The authors cleverly position Chinese demand as likely more of a market distortion than the actions of an informed buyer:

It is entirely possible that the current owners of gold know nothing about the value of gold and only the Chinese know the true value of gold. In that case the current owners of gold will one day regret parting with the gold they sell to the Chinese. Or it could be that Chinese accumulation of gold could ultimately resemble the attempts of the Hunt Brothers to corner the silver market in 1980.

The authors go on to suggest that central banks have essentially colluded to prop up the price of gold. Positive price momentum has further discouraged them from selling gold:

Some Western central banks sought to lighten up on their gold holdings but the lack of liquidity in the gold market forced them into a series of Central Bank Gold Agreements (CBGA). The essence of the CBGAs was that the central banks that wished to sell gold collectively agreed that they would not sell more than some set amount of gold in any one year…The motive for limiting the number of tons of gold sold in any one year was a belief that the gold market could not absorb more gold sales without the price of gold falling significantly.

Just as OPEC attempts to keep oil prices as high as possible by matching supply to demand, the CBGAs were an attempt to prevent the price of gold from collapsing by matching supply to demand. Western country CBGA gold sales have declined substantially over the last few years as the central banks of the Western countries have reassessed the wisdom of selling their gold holdings in an environment characterized by rapidly rising gold prices…The CBGAs focused on limiting the negative price impact of “excess supply.” At the margin, for the last few years the gold market has been impacted by central bank “excess demand” and it is possible that this “excess demand” could persist well into the future.

When the primary purveyors of paper currency are acting in a way consistent with higher gold prices, I want to stay invested.

Conclusion

Finally, the authors conclude:

In the end, investors are faced with a golden dilemma. Will history repeat itself and the real price of gold revert to its long-term mean – consistent with a ‘golden constant’? Alternatively, have we entered a new era, where it is dangerous to extrapolate from history? Those are the uncertain outcomes that gold investors have to grapple with and the passage of time will do little to clarify which path investors should follow.

I was surprised that after all the evidence and analysis the authors provided, they still allowed for a lot of uncertainty in the “passage of time.” The new era explanation is not well-supported by their analysis. Their analysis heavily favors the conclusion that gold is extremely over-valued. For example, the authors estimate that gold as an inflation hedge should be valued around $780 per ounce, a 41% decline from today’s spot price of $1332.

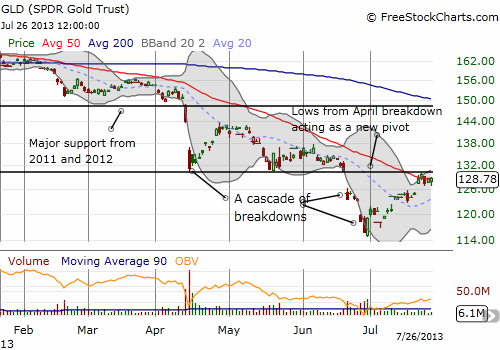

The authors missed a chance to enhance their analysis with an examination into the factors that have driven gold’s price downward for over two years. The sell-off accelerated with a major breakdown the month before the paper was published. The popular reasons offered to explain the sell-off are the same reasons the authors conclude cannot (or should not) help explain the rise in gold’s price. The reasons have adjusted or rotated with each new leg downward, highlighting the difficulty in deriving consistent correlations. My guess is that true gold investors are buying into the sell-off as momentum investors and traders reverse earlier bets.

(click to enlarge)

GLD’s current downtrend is now well-defined by its 50-day moving average (and soon its 200DMA)

Source: FreeStockCharts.com

I am staying in gold because I think ultimately the Federal Reserve will be strongly biased toward keeping real interest rates a lot lower than normal in order to assure itself that an economic recovery is firmly in place. If Janet Yellen replaces Ben Bernanke as Fed chair, then that scenario remains just as, if not even more, likely. The fear of deflation motivates a pro-inflation bias. Inflation may even become an essential tool for managing U.S. debt (although it will be strongly denied). If ever inflation grows roots, I expect the Fed to react slowly and to lose control of it by the time it cares about it, similar to the way in which it handled the stock market bubble of the late 1990s and the housing market bubble that followed. I fully expect gold to “take off” under such a scenario.

I am perfectly happy if no dire scenarios come to pass. We will all be better off if the unprecedented monetary policies of the world’s central banks manage to deliver real economic growth. We should celebrate if they manage to unwind these policies in ways that avoid triggering new financial crises that in turn necessitate yet more accommodative policies. Until that happens, I will keep my bets on gold.