In this article, I explore the effects of a U.S. technical default. By technical default, I mean a delay in making a coupon or principal payment by Treasury because the government fails to raise the debt ceiling. The delay is short term (a few days) and it is viewed by the market as the government’s unwillingness to pay and not its ability.

Even though the odds of a technical default are very small, I would like to discuss its potential effects for gold given what I have read in Credit Suisse’s commodities report. The analysts said recently: “There is, of course, a tail risk that the political divide in Washington becomes so great that Congress fails to raise the debt ceiling in time. That would be disastrous for asset prices of all kinds in our view and we are not convinced that gold would necessarily do well in the mass liquidation/margin call panic that would probably ensue.”

Lehman Brothers 2.0

Theoretically, a technical default would cause a “flight to liquidity” out of government money funds because such funds seek first to preserve the value of the investment at $1.00 per share and second to maintain daily liquidity. As a result, even if a technical default is viewed by the market as temporary and a non-solvency issue, money market funds would have to liquidate portfolio holdings due to extreme redemption pressure from high-risk averse institutional investors, pushing Treasury yields much higher. This is exactly what happened in the aftermath of the Lehman Brothers collapse on September 15, 2008.

Lower redemption pressures were only seen from September 19, 2008, when the U.S. government and the FED took actions by announcing a temporary guarantee of money market funds.

The impact of a .U.S technical default would be much worse than the Lehman Brothers failure. Indeed, while Lehman Brothers owed $517bn when it filed for bankruptcy, the outstanding government debt is today $12tn.

If we look at precious metals during the days following the Lehman Brothers, we can see that the precious metals complex rose significantly due to strong safe-haven demand (PHYS/PSLV). From September 11, 2008 (4 days before the collapse of Lehman Brothers) to September 23 (8 days after the collapse), gold (GLD) surged by 17.44% from $751.30 an ounce to $882.30 an ounce while silver (SLV) rose by 22.81% from $10.740 an ounce to $13.190 an ounce. As seen below, the sharp increase in gold was temporary as gold fell back to pre-Lehman crisis level by mid-October of 2008.

Source: Kitco

The Peru experience of 2000

From a historical perspective, let’s analyze the Peru technical default in September 2000, as it is the most relevant example given the current situation in the U.S. Indeed, contrary to other technical sovereign defaults experienced in the past, the Peru technical default was the only one default not related to a solvency issue.

On September 7, 2000, Peru missed Brady bon coupon payments of $80m due to a legal problem with the hedge fund Elliott Associates (a “rogue” creditor specializing in distressed or bankrupt assets).

On September 29, 2000, Peru settled its case with Elliott by agreeing to pay the full amount set out in the original judgment.

On October 4, 2000, coupon payments were promptly paid to Brady bondholders.

The situation was analogous to what could happen in the U.S. because even though the government missed a payment, investors believed strongly that Peru would not default.

In the case of Peru, Brady bonds spreads rose sharply as a result of uncertainty: spreads climbed 25 basis points to 506 basis points on September 7 (the day of the technical default) and continued to rise to 615 points basis until October 4 (the day of the payment of the coupon).

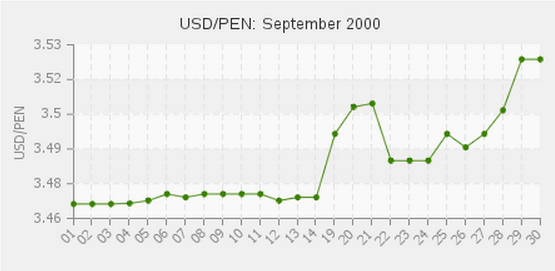

As seen below, if we have a look at the USD/PEN (U.S. dollar/Peruvian Nuevo sol), we can see that USD/PEN rose sharply by 3.56% from 3.4722 on September 7, 2000, to 3.5958 on October 2, 2000, before falling back to pre-technical default crisis level at 3.4977 on October 6, 2000.

(click to enlarge)

(click to enlarge)

Source: Free Currency Rates

Historical lessons

In sum, if the U.S. government temporarily missed a coupon payment, Treasury rates would increase significantly due to a “flight” to liquidity and gold would surge sharply while the dollar would decline in the very short term due to uncertainty and fears similar to what happened following the Lehman Brothers collapse in 2008.