Throughout the gold bull market, we examined the relationship between gold and monetary policy. Analysis of correlation between US real rates and gold prices provided us with an accurate model to predict the gold price until quantitative easing began to have a dominant effect. Once this occurred, we used the influence of the new monetary stimulus to show us the direction of the gold market

Simply put, as economic data weakens the chance of more QE increases. The loosening of monetary policy drove the gold bull market to all-time highs. Conversely, as the employment situation improved the likelihood of more stimulus decreased, as did the chance of gold making new all-time highs.

The last NFP print was weak, the lowest in the last three years. The mechanism described above indicates that this should push gold prices higher, which, over the short-term, we agree with. The weakness is enough to support gold for at least the next month.

(click to enlarge)

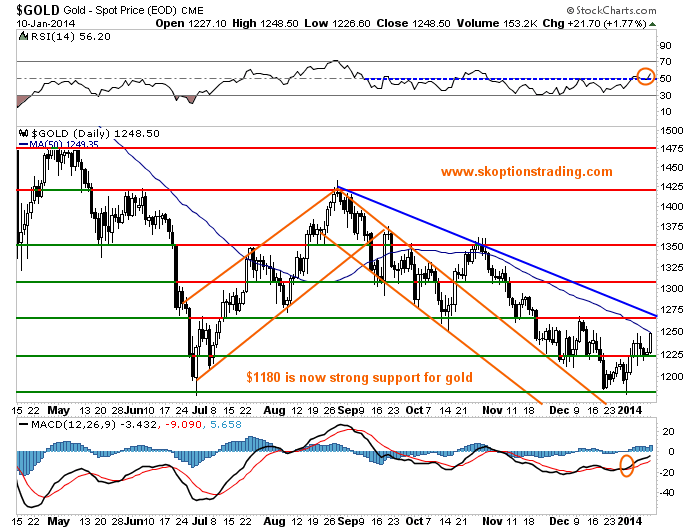

In addition to strength in the fundamentals, the technical situation also looks positive for the yellow metal. A bullish crossover in the MACD has helped fuel a bounce from $1180, which has now become a major support level. A move to 56 in the RSI has shown an improvement in the strength of gold that we have not seen since gold challenged $1350 in October.

When considering these factors, it is highly plausible that gold will make a run to $1275 in near term. If this level breaks, then gold will have moved out of the medium term downtrend it has been in since August, and could then rally above $1300 before the next employment data release. However, beyond the NFP print in February, we must look at the longer-term situation.

The next batch of employment data could reveal the last to be an anomalous result, just as weak the data in July was. If this happens, it will support the Fed’s decision to taper, and, should the print afterwards be strong, it will be probable that QE will be reduced again at the March meeting. Such a scenario will likely see gold falling back to $1180 and lower over the course of the year.

On the other hand, it would take many consecutive poor NFP prints to bring about new quantitative easing, as the Fed would need to see significant deterioration in the economy to take this action. This means that over the long term it makes sense to hold a bearish view on the gold market. A print of 74,000 does not change the overall employment situation as the 12 month average is 182,000 new jobs a month and the 3 month average is 172,000, which are both strong enough to support keeping the taper in place at the next meeting. This will allow two more data releases before the Fed meets again.

(click to enlarge)

Therefore, over the short term we find a small rally in gold to be likely, although we are still bearish overall. The key here is to examine the employment data, whether accurate or not, from the Fed’s point of view. Strong data will mean more tapering and lower gold prices to profit from. Soft prints should lead to greater support for gold, and the potential long trades on the market. As the employment situation changes we will continue to analyze the market and take positions accordingly, just as we have done in the past.