Gold vs. US Dollars

Gold vs. Euros

Gold vs. Ukraine Hyyvnia

It took about 4,000 Hyyvnia to buy an ounce of gold at the end of 2008. It takes 17,444 now.

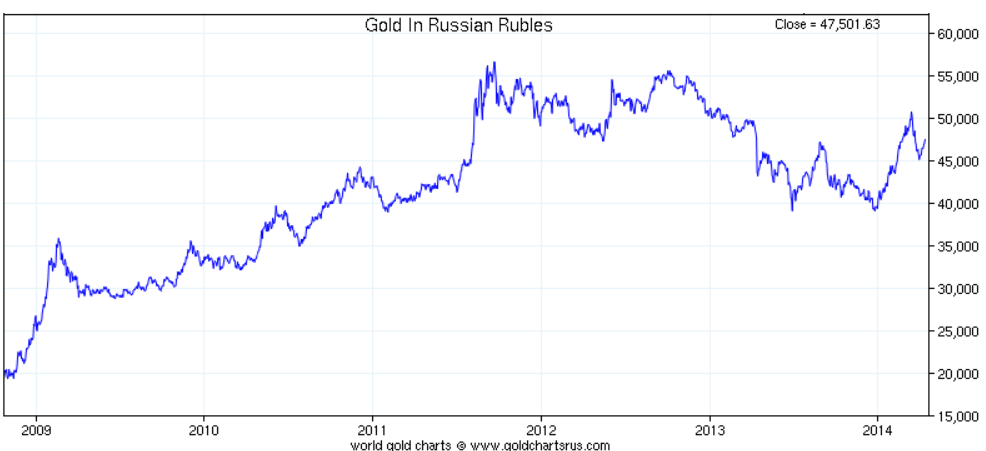

Gold vs. Russia Rubles

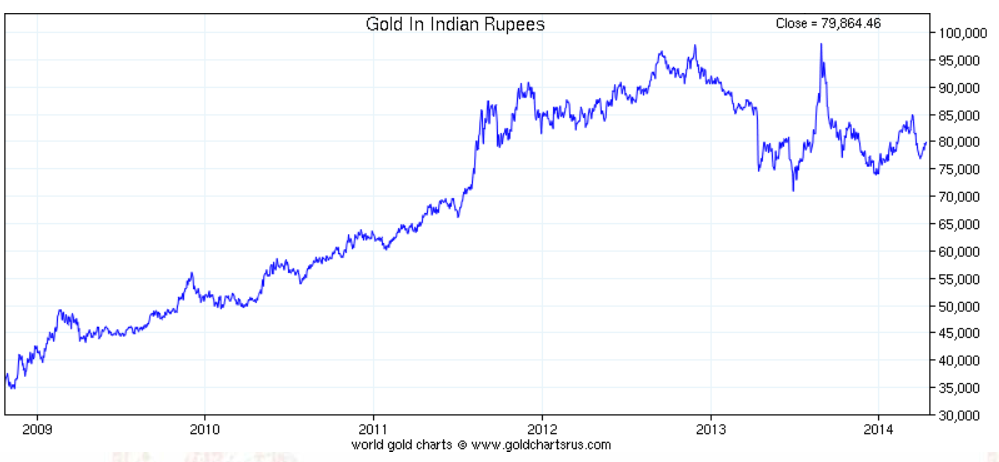

Gold vs. India Rupees

Gold vs. Argentina Pesos

Gold vs. Venezuelan Bolivars

Gold vs. Yen

By the way: Those in Argentina and Venezuela cannot buy gold at the quoted rates. The charts reflect “official” exchange rates. Black market rates are much much higher.

Goldman Sachs and Morgan Stanley Reiterate Sell Signal

Bloomberg reports Goldman Stands by $1,050 Gold Target on Outlook for Recovery

Bullion’s rally this year was spurred by poor U.S. data probably linked to the weather and rising tension in Ukraine, analysts led by Jeffrey Currie wrote in a report, describing the reasons as transient. With the tapering of the Federal Reserve’s bond-buying program, U.S. economic releases will return as the driving force behind lower prices, he wrote.

Gold’s 12-year bull run ended in 2013 as the Fed prepared to reduce monthly bond-buying that fueled gains in asset prices while failing to stoke inflation. Prices rose 10 percent this year even as the Fed cut purchases, with Russia’s annexation of Crimea and mixed U.S. economic data boosting haven demand. Last year, Currie described gold as a “slam-dunk sell” for 2014.

“It would require a significant sustained slowdown in U.S. growth for us to revisit our expectation for lower gold prices over the next two years,” Currie wrote in the report, dated yesterday. “While further escalation in tensions could support gold prices, we expect a sequential acceleration in both U.S. and Chinese activity, and hence for gold prices to decline.”

Gold for immediate delivery traded 0.3 percent higher at $1,322.01 an ounce at 7:43 p.m. in Singapore, according to Bloomberg generic pricing, after the United Nations Security Council met to address the Ukraine crisis. Bullion last traded below $1,050 an ounce in February 2010.

Morgan Stanley

Bullion is the least preferred commodity among metals as prices resume a decline this year on the outlook for rising U.S. interest rates and low inflation expectations, Morgan Stanley said in a report on April 8. Average prices are expected to drop for the next four quarters, it said.

Stronger U.S. growth this year and next will help the world economy withstand weaker recoveries in emerging markets, according to the International Monetary Fund. The world’s largest economy will expand 2.8 percent this year and 3 percent in 2015, unchanged from forecasts in January, the IMF said in its World Economic Outlook report last week.

Least Preferred Commodity?

Is gold really the least preferred commodity? Actually, I hope so, because if it is, sentiment will reverse.

Please consider Gold Prices 2014: Do What Goldman Does, Not What It Says

Jeffrey Currie, the investment bank’s head of commodities research, has repeated his $1,050 target several times since last October, when he declared gold a “slam-dunk sell” along with other precious metals.

But investors need to be very skeptical when looking at Goldman’s forecasts for gold prices. Not only are they often wrong, but the bank frequently does the opposite of what it recommends.

Goldman and Gold Prices: A Shady History

Let’s first look at some of Goldman’s gold price forecasts over the past few years and how they panned out.

For example, back in 2007, Goldman was bearish on gold, telling its clients to sell. In fact, Goldman declared selling gold in 2008 one of its Top 10 tips of the year.

Of course, gold prices rose 12.2% in 2008 and another 23.4% in 2009.

By November 2011, Goldman was actually bullish on gold prices – it raised its target to $1,930 an ounce about one month after gold prices had peaked.

By May 2012, with gold prices below $1,600, Goldman adjusted its bullish target to $1,840 an ounce. Gold prices did rise slightly after that, but never made it to $1,800, and thereafter started a precipitous decline.

By December 2012 – when gold prices were trading in the neighborhood of $1,700, Goldman revised its forecast to $1,800. Six months later gold prices were slipping toward $1,200.

Goldman finally reversed course in February 2013, beginning its string of bearish forecasts that have continued to the present.

That’s actually good news for gold prices, as Goldman always seems to be late figuring out where gold is headed.

Gold Doomed or Resting?

Seldom is sentiment so bad for what is frequent slump in commodities and especially for something that still appears to be a long-term bull market.

When in doubt, it pays to take the opposite side of what Goldman Sachs publicly says. Goldman has a history of not only being wrong, but betting against its own recommendations.